Is Parag Parikh Financial Advisory (PPFAS) Worth Buying at the Current Valuation?

The Indian mutual fund industry is undergoing a structural transformation as household savings continue shifting from traditional assets such as gold and real estate toward financial assets. This trend has created massive opportunities for asset management companies (AMCs), and among them, Parag Parikh Financial Advisory Services (PPFAS) has emerged as one of the fastest-growing players in the industry.

At the current unlisted market price of around ₹17,950 per share, investors are naturally asking whether PPFAS still offers meaningful upside or whether its impressive growth is already reflected in the valuation. To answer that question, it is important to examine the company’s business model, AUM growth, profitability, competitive position, and valuation relative to listed peers.

Understanding the PPFAS Business Model

PPFAS operates primarily through its mutual fund business under the Parag Parikh Mutual Fund brand. In addition to mutual funds, the company also earns revenue through Portfolio Management Services (PMS) and trustee services. However, the asset management business remains the primary growth engine.

During FY25, the company generated approximately ₹429 crore in revenue, of which nearly ₹424 crore came from asset management activities. Trustee services contributed around ₹1.66 crore, while interest income remained negligible. This clearly highlights that PPFAS is essentially a pure-play AMC whose future growth depends on its ability to increase assets under management and attract more investors.

Massive Industry Opportunity Still Ahead

The mutual fund industry itself remains one of the biggest long-term opportunities in Indian financial services.

Industry AUM has grown from roughly ₹12 lakh crore in FY15 to more than ₹74 lakh crore today, representing nearly a six-fold increase over the last decade. Looking ahead, industry estimates suggest that mutual fund AUM could potentially exceed ₹300 lakh crore by 2035.

This means PPFAS benefits from two separate growth drivers:

- Growth of the overall mutual fund industry.

- Expansion of its own market share.

Both factors could support long-term earnings growth.

PPFAS Still Has a Small Market Share

Despite managing over ₹1.6 lakh crore in AUM, PPFAS holds only around 1.9% market share of the Indian mutual fund industry. This suggests a long growth runway as the company can benefit from both industry expansion and market-share gains. For investors wondering whether they can buy PPFAS unlisted shares or whether Parag Parikh unlisted shares are a good long-term investment, the company’s relatively small market share indicates substantial room for future growth

Revenue and Profit Growth Have Been Exceptional

Over the last five years, PPFAS has delivered industry-leading growth, with 67% revenue CAGR and 93% PAT CAGR. These growth rates are significantly higher than most listed AMCs and demonstrate the company’s ability to convert rising AUM into strong earnings growth.

Investor and SIP Growth Reflect a Strong Brand

PPFAS’s investor base has grown from just 1,726 investors in FY14 to nearly 49 lakh in FY25, while SIP accounts increased from 97 to over 28 lakh. This remarkable growth highlights strong investor trust in the Parag Parikh brand and provides a recurring inflow engine for future AUM and revenue growth, making PPFAS one of the most discussed unlisted shares in India among long-term investors.

One Risk Investors Must Watch Closely

While the growth story is impressive, there is one notable concentration risk.

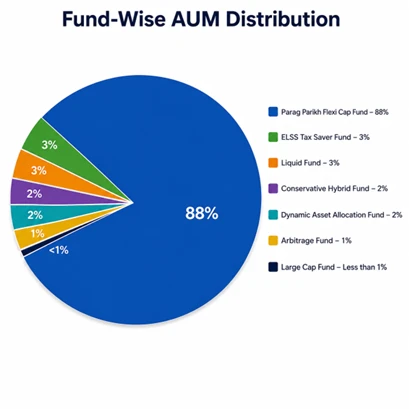

Approximately 88% of the company’s total AUM comes from a single scheme — the Parag Parikh Flexi Cap Fund.

Fund-Wise AUM Distribution

- Parag Parikh Flexi Cap Fund – 88%

- ELSS Tax Saver Fund – 3%

- Liquid Fund – 3%

- Conservative Hybrid Fund – 2%

- Dynamic Asset Allocation Fund – 2%

- Arbitrage Fund – 1%

- Large Cap Fund – Less than 1%

This level of dependence on one flagship fund means any slowdown in fund performance or investor inflows could impact overall business growth.

Operating Leverage Is Driving Profitability

PPFAS has benefited significantly from operating leverage. As AUM has grown, revenue has increased much faster than expenses, resulting in margin expansion. EBITDA margin improved from 47% in FY15 to 79% in FY25, while PAT margin increased from 35% to 57%. Improved cost efficiency has also reduced employee expenses from 37% of revenue in FY14 to 22% in FY25, highlighting the scalability of the business model. For investors researching whether PPFAS is a good buy at the current share price, these improving margins demonstrate the company’s ability to generate strong earnings growth as assets under management continue to expand.

Peer-to-Peer Comparison: Does PPFAS Deserve Its Premium Valuation?

| Metrics | PPFAS | NIPPON | UTI | ICICI AMC | HDFC AMC | ADITYA AMC |

| CMP (₹) | 17950 | 1050 | 915 | 3210 | 2398 | 1068 |

| P/E (x) | 55 | 43 | 25 | 48 | 35 | 31 |

| ROE (%) | 47% | 34% | 10.00% | 85% | 32% | 25% |

| ROA (%) | 43.35% | 31% | 10% | 70% | 30% | 22% |

| ROCE (%) | 63% | 43% | 15% | 115% | 42% | 32% |

| Revenue 5 Year CAGR (%) | 67% | 12% | 7% | 21% | 16% | 9% |

| PAT 5 Year CAGR (%) | 93% | 18% | -1.02% | 21% | 16% | 13% |

| Market Cap (₹ Cr) | 13813 | 67040 | 11789 | 158484 | 102938 | 30866 |

| P/S (x) | 32 | 24 | 6.94 | 26 | 22 | 16.7 |

| EV/EBITDA (x) | 40 | 33 | 13 | 35 | 27 | 23 |

| P/B (x) | 21 | 14 | 2.6 | 38 | 11 | 7.64 |

| EBITDA Margin (%) | 79% | 69% | 48% | 75% | 81% | 58% |

| PEG (x) | 0.6 | 1.56 | 10.6 | 1.65 | 1.38 | 1.84 |

Whenever investors look at PPFAS, the first reaction is usually the same: “The stock looks expensive.” At 55x earnings, 21x book value, and 40x EV/EBITDA, the company is undoubtedly trading at a premium compared to most listed AMCs. This often leads investors to question whether PPFAS is overvalued or whether the company’s strong growth justifies its premium valuation.

However, valuation should never be analyzed in isolation. The key question is whether PPFAS deserves this premium based on its growth, profitability, and business quality. For investors conducting a PPFAS valuation analysis, understanding the relationship between growth and valuation is far more important than looking at valuation multiples alone.

Return Ratios: Why PPFAS Stands Out Among India’s Top Asset Management Companies

Before evaluating valuation, it is important to assess business quality. PPFAS generates an impressive 47% ROE, compared to 34% for Nippon AMC, 32% for HDFC AMC, and 25% for Aditya Birla AMC. Similarly, the company delivers a 43% ROA versus 31% for Nippon AMC and 30% for HDFC AMC, while its 63% ROCE is substantially higher than 43% for Nippon AMC and 42% for HDFC AMC. These metrics place PPFAS among the most profitable and capital-efficient AMCs in India, second only to ICICI AMC on most return parameters, highlighting the company’s strong business economics and efficient capital allocation. Such strong return ratios help explain why PPFAS is increasingly being discussed as a potential pre-IPO investment opportunity among long-term investors.

Growth: The Biggest Reason Behind PPFAS’s Premium Valuation

PPFAS’s premium valuation is primarily driven by its exceptional growth. Over the last five years, the company has delivered 67% revenue CAGR and 93% profit CAGR, significantly outperforming listed peers such as HDFC AMC and ICICI AMC. With revenue growing 3–4 times faster and profits growing 5–6 times faster than most AMCs, the market is willing to assign a higher valuation multiple to the company.

P/E Ratio: Is 55x Earnings Too Expensive?

PPFAS trades at around 55x P/E, compared to the AMC sector average of 36x, implying a premium of nearly 51%. While the valuation appears expensive, it reflects the company’s superior growth, profitability, and earnings compounding ability. For investors evaluating the PPFAS pre-IPO investment opportunity, the key question is whether this earnings premium can be sustained through continued AUM growth and market-share gains.

EV/EBITDA: Premium Supported by Strong Fundamentals

PPFAS trades at approximately 40x EV/EBITDA versus the industry average of 26x, representing a premium of around 52%. The premium is supported by rapid AUM growth, rising SIP inflows, and strong operating leverage, which is why many long-term investors continue to track PPFAS as a high-growth unlisted investment opportunity

Price-to-Sales: The Highest Premium

PPFAS trades at around 32x sales, compared to the peer average of 19x, implying a premium of nearly 67%. This premium reflects the company’s industry-leading revenue growth and the market’s expectation that PPFAS will continue to grow significantly faster than most listed AMC peers, reinforcing its position among the best unlisted shares to buy for long-term investors.

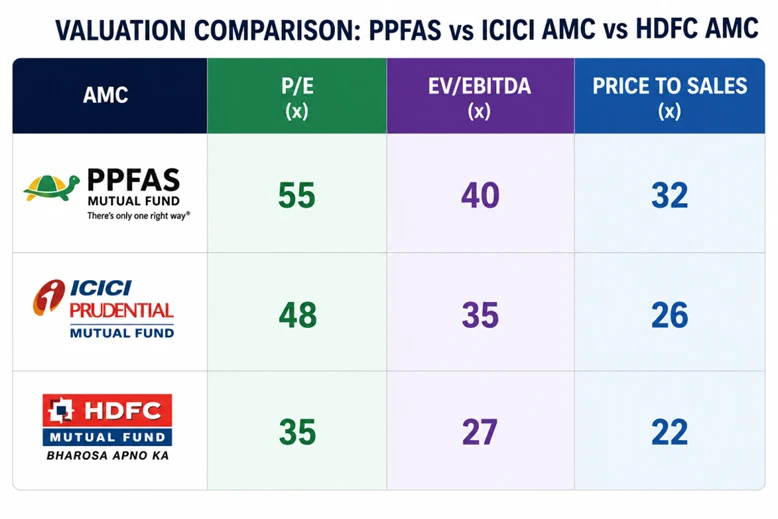

Comparing PPFAS with HDFC AMC and ICICI AMC

A better comparison for PPFAS is with premium AMC players such as HDFC AMC and ICICI AMC. PPFAS trades at 55x P/E, compared to 48x for ICICI AMC and 35x for HDFC AMC, implying a premium of 15% and 57%, respectively. Similarly, PPFAS trades at 40x EV/EBITDA versus 35x for ICICI AMC and 27x for HDFC AMC, while its Price-to-Sales ratio of 32x compares with 26x and 22x for ICICI AMC and HDFC AMC.

Although PPFAS trades at a premium across valuation metrics, it has delivered significantly stronger growth, with 67% revenue CAGR and 93% profit CAGR over the last five years, far ahead of both peers. This superior growth is the primary reason the market assigns a higher valuation multiple to PPFAS.

The PEG Ratio: The Most Important Metric Investors Are Ignoring

While P/E receives most of the attention, PEG is often a better valuation metric for high-growth companies because it adjusts valuation for growth.

PEG Comparison

- PPFAS: 0.60

- HDFC AMC: 1.38

- Nippon AMC: 1.56

- ICICI AMC: 1.65

- Aditya AMC: 1.84

- UTI AMC: 10.60

This is where the valuation story changes dramatically. Despite trading at higher headline valuation multiples, PPFAS has the lowest PEG ratio among its peers. This suggests that investors are paying less for each unit of growth compared to most listed AMCs, strengthening the case for PPFAS as a high-growth unlisted investment opportunity.

Conclusion

Parag Parikh Financial Advisory Services (PPFAS) has emerged as one of the fastest-growing asset management companies in India, supported by exceptional AUM growth, a rapidly expanding investor base, strong SIP inflows, and industry-leading profitability. Over the last five years, the company has delivered a revenue CAGR of 67% and a profit CAGR of 93%, significantly outperforming most listed AMC peers.

While the stock trades at a premium valuation across metrics such as P/E, P/B, EV/EBITDA, and Price-to-Sales, the premium is backed by superior growth, strong return ratios, and a scalable business model. The company’s low market share of approximately 1.9% also suggests that a significant growth runway remains as India’s mutual fund industry continues to expand. For investors looking to explore unlisted shares with strong fundamentals, proven execution, and long-term growth potential, PPFAS remains a company worth tracking closely.

Why Choose The Unlisted Network?

- Investing in unlisted shares requires more than just access to opportunities—it requires transparency, research, and execution support.

- Transparent Pricing: No hidden markups or surprise charges.

- Research-Driven Insights: Detailed company analysis, valuation frameworks, financial breakdowns, and industry research.

- Access to High-Quality Unlisted Opportunities: Explore leading pre-IPO, startup, and unlisted investment opportunities through a single platform.

- Structured Transaction Process: End-to-end support from price discovery and documentation to share transfer and settlement.

- Investor-Focused Approach: Helping investors make informed decisions through data-backed research and insights.

Final Note

PPFAS may appear expensive on traditional valuation metrics, but valuation should always be viewed alongside growth. Few financial services businesses in India have been able to compound revenue, profits, and AUM at the pace PPFAS has demonstrated over the last decade. The company’s strong brand, growing distribution network, expanding investor base, and long runway within India’s mutual fund industry position it well for future growth.

For long-term investors, the key question is not whether PPFAS trades at a premium today, but whether it can continue growing significantly faster than the industry over the coming years. If the company maintains its execution track record and continues gaining market share, the current valuation premium could prove justified. For investors looking to invest in unlisted shares backed by strong fundamentals, scalable business models, and long-term growth potential, PPFAS remains a company worth tracking closely.

Disclaimer: This article is for informational and educational purposes only and should not be considered investment advice. Investors should conduct their own research and consult a qualified financial advisor before making any investment decisions.